Minera Alamos Announces Positive Preliminary Economic Assessment for the La Fortuna Gold Project with After-Tax IRR of 93%

Minera Alamos Inc. [TSXV: MAI] is pleased to announce the positive results of an independent Preliminary Economic Assessment for its La Fortuna Project in Durango, Mexico. The PEA was prepared in accordance with National Instrument 43-101 Standards of Disclosure for Mineral Projects by CSA Global Geosciences Canada Ltd of Toronto, Canada. (Note to reader: Unless stated all currency references are in US dollars).

Notes:

1. GEO – Gold Equivalent Ounces

2. “AISC per ounce” is a non-GAAP financial performance measures with no standardized definition under IFRS; additional reference info at bottom of release

3. Base case prices for gold, silver and copper were assessed at values approximately 2%-7% below the three-year trailing average prices for each of the metals and below the majority of the publicly available forward looking estimates available as of July 2018

PEA Cautionary Note:

Readers are cautioned that the PEA is preliminary in nature and there is no certainty that the PEA results will be realized. Â Mineral resources are not mineral reserves and do not have demonstrated economic viability. Â Additional work is needed to upgrade these mineral resources to mineral reserves.

“With an after-tax Internal Rate of Return in excess of 90%, today’s excellent PEA results confirm that the La Fortuna Project provides a robust base for the next phase of gold production in the Company’s growth pipeline,” commented Darren Koningen, Chief Executive Officer.  “The simplified gold recovery process outlined in the study represents a conservative starting point that is well suited to the initial project resource which, to date, has been based exclusively on previously drilled mineralization. As our engineering work progresses we continue to find opportunities to reduce the initial project capital requirements and improve overall project economics.  Coupled with our strategic partnership with Osisko Gold Royalties that includes an option to provide a significant portion of the project capital requirements in return for a Project royalty, these additional optimizations will greatly reduce the upfront funding requirements of this already low capital cost operation.”

“This PEA represents a key milestone for the Company as we begin to deliver to the market’s attention the underlying project economics of our development pipeline that focuses on cost-efficient and targeted production that can incrementally build a significant production profile over time,” commented Doug Ramshaw, President. “With the recently submitted commercial permit applications at the Santana project and ongoing work at the Company’s Guadalupe de los Reyes project we are aggressively expanding our activities on multiple fronts.  We continue to envision a plan whereby targeted production from the development of the Santana project will support the modest capital requirements of the La Fortuna operation.”

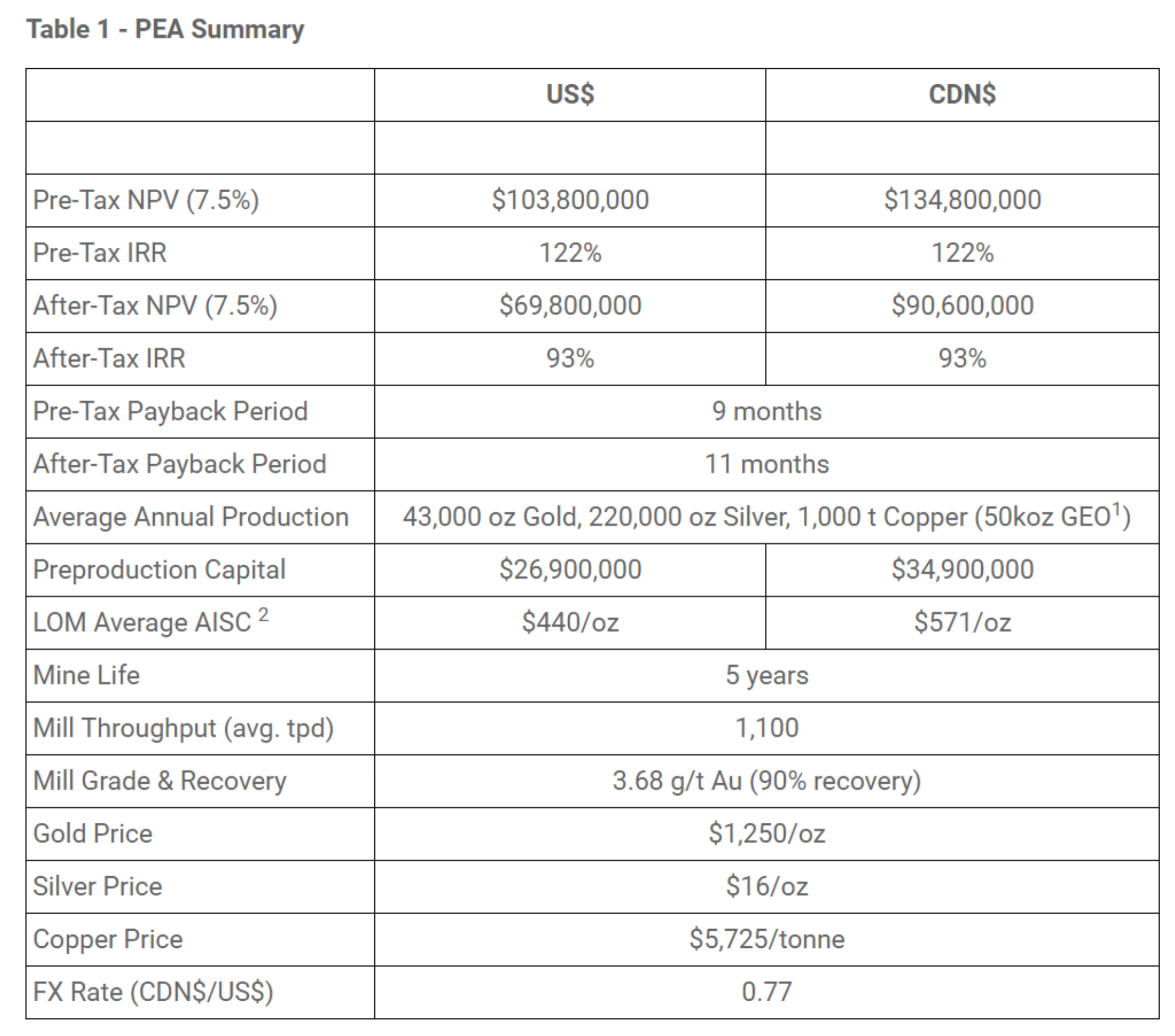

Production and Economic Highlights

Production highlights

- Average annual contained-metal production of approximately 50,000oz Gold Equivalent (43,000oz Gold, 220,000oz Silver, 1,000t Copper).

- 5-year mine life based on initial resource “starter pit” with 2.0 Mt of mineralization (3.68 g/t Au, 20 g/t Ag, 0.27% Cu) processed at 1,100 tpd average processing rate.

- 215koz of Gold, 1.1Moz of Silver, and 5kt of Copper produced in concentrates.

Robust economics using metals prices of $1,250/oz Au, $16/oz Ag, and $5,725/t Cu:

- All-In Sustaining Cost (AISC) of $440/oz [net of by-product credits]

- After-Tax NPV at 7.5% of $69.8M and IRR of 93%.

- Pre-Tax NPV at 7.5% of $103.8M and IRR of 122%.

Low initial capital costs and rapid payback:

- Pre-production capital costs of $26.9M.

- Payback period of 11 months.

- 2,000 t/d mill already purchased awaiting shipment to site reduces up-front capital.

Significant Upside:

- Current PEA completed on project “starter pit” resource only, a single zone of drilled mineralization that appears to remain open geologically.

- Additional milling capacity – project permitted for a 2,000 tpd operation with the PEA based on a starting rate of 1,100 tpd.

- Numerous opportunities for significant economic improvement – improved gold recoveries, reduced initial capital costs, etc.

For complete report and table click here.