Price Recovery Looks Sustainable As Copper Demand Escalates

Consumer recognition of various metals, their usage, and how they impact their personal lifestyles generally tends to be quite limited in the general population. However, most consumers are familiar with copper and the metal’s usage in both personal and commercial applications.

Most people taking basic high school chemistry know that copper has the chemical symbol Cu and is a reddish-orange metal that oxidizes to green on the roofs of some of the country’s most venerable hotels – the Hotel Vancouver being one of the better examples. International mining company and copper producer, Vale, describes the metal as “malleable, resistant to corrosion and high temperatures, recyclable and blessed with the best electrical and thermal conductivity of any commercial metal.”

“Copper is highly valued for its application in power transmission and generation, building wiring, as well as practically all electronic equipment including mobile phones and television sets,” the company notes.

According to Vale, copper is the third most used metal in the world after iron and aluminum. Approximately 66% of the copper consumed every year is used in electrical applications but it has many other uses as well – some of historic significance. Almost 73 metric tonnes of copper sheeting were used to create the Statue of Liberty’s skin in New York harbour. Marrying copper with zinc produces brass, an alloy more malleable and with better acoustic properties than either of the metals alone; copper is largely employed around the home thanks to its antimicrobial properties – the better to reduce the transfer of germs. Today, universities are working to identify “copper eating” bacteria and fungi capable of absorbing copper from mine tailing dams – research that has the potential to significantly boost copper recovery from waste while revolutionizing the industry in the process. Vale is funding research in this area.

Teck Resources, which produces copper at its Highland Valley operation in central BC and at operations in South America, notes the refined copper market reached record highs in the second quarter, with prices hitting US$4.78 per pound in mid-May. Demand outside of China continued to recover through the first half of 2021 while demand within China moderated into the slower summer season. Demand for refined copper and related products has now surpassed pre-COVID-19 levels. This was partly the result of government stimulus measures, pent up demand for consumer goods, logistics bottlenecks, increased infrastructure spending and improved construction and manufacturing activities.

Tightness in the copper concentrate market continued into the second quarter, with spot treatment charges remaining below the annual negotiated contract terms for 2021. Reported mine production disruptions in the second quarter have been relatively minor and mine production is starting to return to pre-COVID-19 levels, according to Teck. Nonetheless, risks to production still remain as health authorities in various jurisdictions continue to enact measures to limit the spread of COVID-19.

Furthermore, the company reports that spot treatment charges rose through the second quarter as several smelters took scheduled maintenance outages during the quarter. Premiums for copper cathode in China remained under pressure as buyers continued to source cheaper scrap alternatives, as scrap availability increased with rising prices.

In addition, South American mine production, which accounts for the majority of global output, improved significantly in the second quarter compared to a year ago primarily due to the Covid19 lockdowns which occurred in the second quarter of 2020. South American mine production to the end of May 2021 was still below pre-COVID-19 levels as supply constraints continued to impact production. Exports from South America to the end of May 2021 were down 5.5% year-over-year from 2020 and were also 13.8% lower versus the same period in 2019, the company advises.

Copper prices quoted on the London Metal Exchange (LME) are important to all producers including Teck which notes the price averaged US$2.80 per pound in 2020, up from an average of US$2.72 per pound in 2019. Copper stocks on the LME fell by 26% to 107,950 tonnes in 2020, and copper stocks on the Shanghai Futures Exchange fell by 30% to 86,700 tonnes, while COMEX warehouse stocks rose 120% to 68,400 tonnes. Combined exchange stocks decreased by 38,500 tonnes during 2020 and ended the year at 261,700 tonnes, or less than four weeks of global consumption, well below the 25-year average of 11.3 weeks of global consumption, Teck confirms.

Newsletter, Market Trading Essentials, reports that copper stocks represented by the Global X Copper Miners ETF (COPX) have outperformed the broader market by a wide margin. In fact, COPX has provided a total return of 132.7% over the past 12 months, nearly four times the Russell 1000’s total return of 34.7%.

Teck also notes that copper’s sharp uptick saw it almost double in price from its Covid-fueled lows, the result of a widely-held belief that demand for the bellwether metal will receive a massive boost, not just from post-pandemic economic stimulus but also from a worldwide push for de-carbonization.

Exchange stocks ended the year at six-year lows and came within 1,000 tonnes of reaching levels last seen in 2008. Total reported global stocks, including producer, consumer, merchant and terminal stocks, stood at an estimated 18.8 days of global consumption versus the 25-year average of 26.9 days, the company adds.

In 2020, global copper mine production decreased 1.4% according to Wood Mackenzie, a commodity research consultancy, with total production estimated at 20.6 million tonnes. The consultancy is forecasting a 3.5% increase in global mine production in 2021 to 21.3 million tonnes.

Copper scrap availability decreased in 2020 as scrap and unrefined copper imports into China, including blister and anode, were down 5.9% year-over-year to December 2020. China-refined copper imports increased by 36% in 2020 to 4.3 million tonnes in response to improved demand, inventory restocking, and lower availability of copper concentrates and copper scrap.

Wood Mackenzie estimates that global refined copper production grew 1.0% in 2020, above the 1.3% decrease in global copper cathode demand. They are projecting that refined production will increase 1.5% in 2021, reaching 24.1 million tonnes.

The fundamentals for copper will improve in the coming years as global stimulus spending by governments continues, and as governments and corporations continue to build out their exposure to the green economy through increased electrification and reductions to carbon emissions, requiring additional copper units, Teck predicts.

According to Teck, copper concentrate and copper matte are intermediate products in the copper production chain. Both the concentrate and matte markets are competitive, having numerous producers but fewer participants and smaller volumes than in the copper cathode market due to the high levels of integration by the major copper producers. In the copper concentrate market, mining occurs on a global basis with a predominant share from South America, while consumers are custom smelters located mainly in Europe and Asia.

The company’s competition in the custom copper concentrate market occurs mainly on a global level and is based on production costs, quality, logistics costs and reliability of supply. Its largest competitors in the copper concentrate market are Freeport McMoRan, Glencore, BHP Billiton, Codelco, Anglo American, Antofagasta plc, Rio Tinto and First Quantum, each operating at the parent-company level or through subsidiaries.

Vale describes the global refined copper market as being highly competitive, noting that producers are integrated mining companies with custom smelters covering all regions of the world while consumers are principally wire rod and copper-alloy producers. Competition occurs mainly on a regional level and is based primarily on production costs, quality, reliability of supply and logistics costs.

Among the world’s largest copper cathode producers are Vale competitors: Jiangxi Copper Corporation Ltd., Corporacion Nacional del Cobre de Chile (‘‘Codelco”), Tongling Non-Ferrous ´ Metals Group Co., Freeport McMoRan Copper & Gold Inc., Aurubis AG and Glencore.

Wood Mackenzie is forecasting that global copper metal demand will increase by 2.7% in 2021, reaching 24.0 million tonnes, suggesting the refined copper market will be balanced in 2021.

In the meantime, Codelco, the Chilean state-owned copper mining company, reports positive data from the Chinese economy in July showing its economy grew more than expected during the second quarter, encouraging investment funds to consider metals such as copper, zinc and nickel in their investment strategy. At the time, Chinese public spending sustained part of the growth of copper-intensive sectors which included more investment in infrastructure and increased domestic consumption that was reflected in higher retail sales.

Codelco saw its sales surge last quarter as the world’s biggest copper supplier ramped up production just as rebounding economies sent prices of the metal to record highs. The company’s chairman, Juan Benavides, told Bloomberg and other media outlets that copper prices are likely to remain strong given growth in the United States, Southeast Asia and China, while cautioning that the spread of Covid19 variants could spark fresh volatility in the market.

Chilean copper agency, Cochilco, has significantly increased its copper price forecasts for this year on expectations of a short-term deficit in the global market. In fact, Cochilco has raised its average copper price projection to $4.30/lb for 2021, up from a forecast of $3.30/lb that was made in January.

An expected supply deficit in the short term, along with reduced inventories in metal exchanges, will provide fundamental price support, Cochilco executive vice-president Marco Riveros predicts. By the end of 2021, the refined copper market is expected to be in a deficit of 145,000t while at the end of 2022 a surplus of 46,000t is forecast.

As reported in Argus Media, Riveros said the macroeconomic scenario for the rest of 2021 of the main copper-consuming economies is positive for the demand. In addition, global mined copper production is anticipated to grow by 2% on an annual basis this year to 21 million tonnes because of a widespread recovery in the leading copper-producing countries. In Chile, output is projected to increase by 1.8% on the year to 5.8 million tonnes.

Strong future demand for copper will necessitate the development of new mines from the world’s existing inventory of undeveloped deposits which are inherently higher cost than existing producers due to lower grades, higher strip ratios and higher development costs. Analysts foresee that bringing on higher cost mines to meet increasing demand, in conjunction with the long timelines associated with permitting and obtaining social license for new greenfield mines, leading to a prolonged period of higher copper prices.

Two such companies making strides to meet future copper demands are Spruce Ridge Resources Corp. and Capella Minerals Ltd.

Spruce Ridge Resources Ltd. [SHL-TSXV] is a Canadian mineral exploration company that offers investors exposure to high-grade copper in Newfoundland and near-term cash flow from oil and gas properties in Saskatchewan.

Spruce Ridge Resources Ltd. [SHL-TSXV] is a Canadian mineral exploration company that offers investors exposure to high-grade copper in Newfoundland and near-term cash flow from oil and gas properties in Saskatchewan.

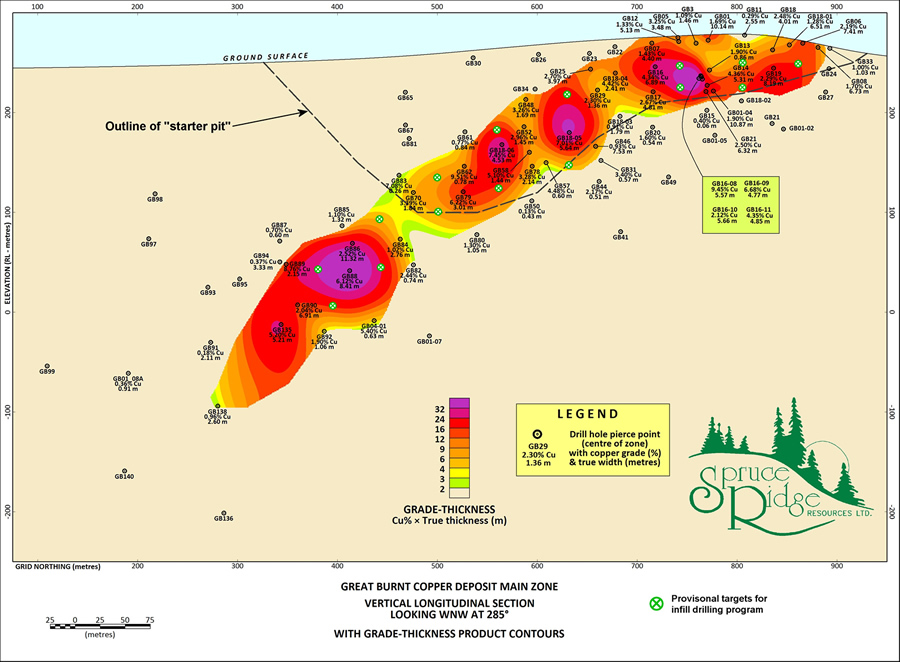

The company’s flagship property is a 100%-owned volcanogenic massive sulphide (VMS) deposit, which is located on a highly prospective base-metals rich greenstone belt in a hot exploration area in central Newfoundland.

Great Burnt consists of four prospective zones, including the Great Burnt, South Pond A, South Pond B, and End Zone Prospect. The project is located 40 kilometres southeast of Teck Resources Ltd.’s [TECK.B-TSX, TECK.A-TSX, TECK-NYSE] Duck Pond mine and 2,000 tonne-per-day concentrator. Â It is accessible via road and airport.

The property emerged on investor radar screens back in April, 2016, when Spruce Ridge reported “surprisingly” high copper grades while drilling on the project’s Main Zone. The four holes were drilled to twin early holes that were drilled by Celtic Minerals in 2001.

Three of the four holes returned average copper values that were more than twice, and up to 3.6 times above the expected grade. Drill intersections ranged up to 9.45% copper, 0.36 g/t gold, 0.73% zinc and 8.5 g/t silver over a core length of 7.50 metres.

Not only were the copper grades higher than expected, but drilling also returned gold, zinc and silver, none of which had been previously considered present in economically significant quantities in the Great Burn Copper Deposit.

Infill drilling on the Great Burnt deposit in 2016 and 2018 resulted in an increase in the inferred resource to 550,000 tonnes of 2.66% copper (32.3 million pounds of contained copper). The inferred resource now stands at 572 million tonnes of 2.41% copper or 30.4 million pounds.

Recent drilling results announced in March 2021, have confirmed the company’s view that historical drilling in the 1960s, tended to understate the copper grades at the Great Burnt.   Highlights of the drilling includes Hole GB20-05 which intersected 27.2 metres averaging 8.02 per cent copper, including 7.75 metres of 16.88 per cent copper, which in turn included 2.0 metres of 21.25 per cent Cu and Hole GB20-20 intersected 22.75 metres of 6.89 per cent copper, 0.79 per cent zinc and 0.05 gram per tonne gold, including 12.55 metres of 10.59 per cent copper, 1.27 per cent zinc and 0.07 gram per tonne gold, which in turn included 1.50 metres of 18.15 per cent copper, 1.98 per cent zinc and 0.04 gram per tonne gold. The GB20-20 intercept is 187 metres north and 108 metres higher than the previously reported intercept in hole GB20-05.

Recent drilling results announced in March 2021, have confirmed the company’s view that historical drilling in the 1960s, tended to understate the copper grades at the Great Burnt.   Highlights of the drilling includes Hole GB20-05 which intersected 27.2 metres averaging 8.02 per cent copper, including 7.75 metres of 16.88 per cent copper, which in turn included 2.0 metres of 21.25 per cent Cu and Hole GB20-20 intersected 22.75 metres of 6.89 per cent copper, 0.79 per cent zinc and 0.05 gram per tonne gold, including 12.55 metres of 10.59 per cent copper, 1.27 per cent zinc and 0.07 gram per tonne gold, which in turn included 1.50 metres of 18.15 per cent copper, 1.98 per cent zinc and 0.04 gram per tonne gold. The GB20-20 intercept is 187 metres north and 108 metres higher than the previously reported intercept in hole GB20-05.

In July 2021 Spruce Ridge received the results of an updated mineral resource estimate for the Great Burnt copper and gold property. The most prominent change is the increase in copper grades of the Main zone, from 2.66 per cent copper to 3.21 per cent copper in the indicated classification, with a smaller decrease from 2.41 per cent copper to 2.35 per cent copper in the inferred classification. There was a matching increase in the contained copper content from 32.3 million pounds (indicated) plus 30.4 million pounds (inferred) to 47.2 million pounds (indicated) plus 25.0 million pounds (inferred).

The mineral resource estimate was prepared by P&E Mining Consultants Inc. It will be used in a preliminary economic assessment (PEA), expected to be completed later this year. Core samples from the 2020 diamond drilling program were sent to SGS in Lakefield, Ont., for beneficiation testing.  Metallurgical testing by SGS, as well as external test work using sorting technology, is now under way.

The mineral resource estimate was prepared by P&E Mining Consultants Inc. It will be used in a preliminary economic assessment (PEA), expected to be completed later this year. Core samples from the 2020 diamond drilling program were sent to SGS in Lakefield, Ont., for beneficiation testing.  Metallurgical testing by SGS, as well as external test work using sorting technology, is now under way.

Meanwhile, work has begun on the access trail from Great Burnt zone to South Pond B Gold Zone and continue on to the South Pond A Copper/Gold Zone. Â Once the trail reaches the South Pond B Gold Zone, drill sites will be cleared and drilling will commence.

Spruce Ridge CEO John Ryan said the decision was prompted by recent discoveries by New Found Gold Corp. [NFG-TSXV] and others. Â He said the discoveries have highlighted the potential of the Paleozoic sedimentary and intrusive rocks of Central Newfoundland to host substantial zones of high-grade gold.

Spruce Ridge has an option agreement with Magna Terra Minerals Inc. for both its Viking and Kramer gold properties situated near the communities of Pollard’s Point and Sop’s Arm in White Bay, Newfoundland.

In February, 2020 Spruce Ridge sold its interest in the Crawford Nickel-Cobalt Sulphide project in Northern Ontario to Canada Nickel Corp. [CNC-TSXV]. Spruce received shares of Canada Nickel and Noble Mineral Exploration. The Company recently announced that it will dividend out 2,500,000 shares of Canada Nickel leaving a balance of 5,600,000 shares.

The company expects to generate positive cash flow from the recently acquired oil and gas wells in southwestern Saskatchewan from Repsol Canada Energy Partnership

The company said current crude prices will allow it to start producing from five to seven oil wells with relatively low start-up costs.

Spruce Ridge has retained ground in the Crawford Twp area which feature a number of geophysically- defined targets with potential for VMS and gold mineralization.

Proximity to Glencore’s Kidd Creek zinc-copper-silver mine, one of the world’s largest VMS deposits at 100 million tonnes plus enhance the prospectivity of the Crawford Twp area, the company has said.

Spruce Ridge has formed a joint venture with a private group of knowledgeable mining investors to explore VMS and gold targets on its Crawford Twp property.

On August 30, 2021, Spruce Ridge shares were trading at $0.11 cents in a 52-week range of 22.5 cents and $0.065, leaving the company with a market cap of $19.5 million, based on 177.5 million shares outstanding.

Capella Minerals Ltd. [CMIL-TSXV, N7D2-FRA] is a Canadian gold-copper exploration and development company with highly-prospective properties located in favourable jurisdictions in Canada and Scandanavia.

Capella, formerly known as New Dimension Resources, cemented its diversification strategy in August, 2020, by executing an option and purchase agreement with EMX Royalty Corp [EMX-TSXV, NYSE American] for the acquisition of 100% interests in the Southern Gold Line Project in Sweden, and the Lokken and Kjoli copper-zinc-gold projects in Norway.

Southern Gold Line is a relatively early-stage project sitting in a belt with multiple deposits. Covering 500 square kilometres, the project consists of a group of licences adjacent to Dragon Mining Ltd.’s Faboliden gold development project and Svartliden gold mine. Further to the north of Svartliden lies the Barsele gold project, currently an Agnico Eagle Mines Ltd. [AEM-TSX, AEM-NYSE] /Barsele Minerals Corp. [BME-TSXV] joint venture. (300,000 ounces indicated resource and 2.0 million ounces of inferred resources).

The Lokken and Kjoli licenses cover past-producing, high-grade copper (zinc-gold) mines as well as drill-ready regional exploration targets.

Lokken is considered to be the largest ophiolite-hosted Cyprus-type volcanogenic massive sulphide (VMS) deposit to be developed in the world. Production commenced in 1654, and continued until closure in 1987, producing 24 million tonnes at 2.3% copper and 1.8% zinc (plus gold and silver credits), with multiple satellite bodies of mineralization that also saw varying degrees of development.

The Kjoli project contains the Killingdal mine, which operated from 1674 to 1986 and produced over 2.9 million tonnes at 1.7% copper, 5.5% zinc plus the former Kjoli mine (reported mine grades of 2.9% Cu)

Mining operations closed in the mid-1980s when copper was trading at around US60 cents a pound and investor attention in Norway switched to off-shore oil discoveries.

In an interview, Capella President and CEO Eric Roth said the company acquired the Scandinavian projects in the belief that Norwegian geological environment is basically an extension of fabled copper mining camps in northeastern Canada, including the Bathurst and Buchans mining districts.

VMS deposits typically occur in clusters. “Where you find one, you will always find others. That is just the nature of the beast,” Roth said.

The company said recent airborne geophysical surveys identified numerous exploration targets on the Kjoli project that have not yet been followed up.

The long history of mining in Norway, means that exploration companies can benefit from mining related infrastructure, competitive tax rates, low-cost hydroelectric power, and absence of government royalties.

In Canada, Capella is engaged in joint ventures with Ethos Gold Corp [ECC-TSXV]Â at Savant Lake, Ontario, and Yamana Gold Inc. [YRI-TSX, AUY-NYSE] at Domain, Manitoba.

Domain is a high-grade iron formation and shear hosted gold project held 70.4% by Yamana and 29.6% by Capella. It is an advanced stage project with 62 holes (9,660 metres) of diamond drilling completed. Roughly 800 metres of strike has been partially tested at the “Main Zone.” Roughly 5.0 kilometres of prospective strike extensions remain to be tested.

The Savant Lake property covers 230 square kilometres in northwestern Ontario. Ethos has an option to earn a 70% interest in that project by undertaking staged work commitments worth $2 million. Field crews have been mobilized at site and the plan is to drill in the second half of the year.

Capella also retains a residual interest (subject to an option to purchase agreement with Austral Gold Ltd. [AGLD-TSXV] in the Sierra Blanca gold-silver project in Santa Cruz, Argentina.

The company is working towards diamond drilling on four projects by late 2021, including Savant Lake, Domain Gold, and the Lokken & Kjoli copper projects.

However, undrilled VMS deposits in Norway will be the top priority.

In Norway, the company takes the view that the best places to find a new mine is in the shadow of a head frame.

Capella’s management team has a wealth of technical and market experience, and a proven track record of success in finding, growing and advancing mineral discoveries.

Roth is a former chief operating officer of Mariana Resources, which was acquired by Sandstorm Gold Ltd. [SSL-TSX, SAND-NYSE American] in 2017. He is also a non-executive director of Ivory Coast-focused Awale Resources Ltd.

Four major shareholders, hold about half of Capella’s shares. Management has about 9.7%, Sandstorm Gold has 12.9%, EMX Royalty Corp. has 9.9%, and Austrian private group Fruchtexpress Grabher GMBH 15.1%.

On August 24, 2021, Capella announced that it had entered in to a binding Letter of Intent (“LOI”) with ASX-listed Cullen Resources Limited (“Cullen”) through which the Company may earn-in to Cullen’s Katajavaara and Aakenus gold(-copper) projects in the highly-prospective Central Lapland Greenstone Belt (“CLGB”) of northern Finland. The Katajavaara and Aakenus projects lie immediately adjacent to the productive Sirkka Thrust Zone, a regional structural corridor within the CLGB which is associated with numerous occurrences of both gold and base metals.

Capella shares were trading at $0.095 in a 52-week range of 12 cents and $0.065, leaving the junior with a market cap of $14.3 million, based on 151.1 million shares outstanding.

Aside from the property assets, Capella also has shareholdings in Cerrado Gold Ltd. [CERT-TSXV, CRDOF-OTCQX] (833,334 common shares) and Ethos Gold Corp. (2.0 million common shares).