Battery Minerals poised for increased demand with dozens of new EVs planned

By Ron Hall

In our update on May 5 this year we noted that the all mining and metals industries had been hit hard by the onset of a bear market inspired by the COVID-19 pandemic. At that time the Venture Exchange was beginning to recover from a huge drop to around 330. That recovery has continued with the Venture Exchange now at the 720 mark.

Whilst the battery sector, which includes lithium, vanadium, copper, cobalt, nickel, lead, manganese and graphite, remains robust as the increase in demand for smartphones, tablets, and other electronic devices, a rise in call for electrical vehicles/hybrid electric vehicles/plug-in hybrid vehicles, and rapid development in the renewable energy sector continue to drive the longer term growth of the market, the near-term outlook is somewhat bleaker.

Lockdown measures, lower oil prices and tightened household budgets conspired to drop global EV sales in 2020 from healthy growth of 20% to a 13% contraction. This has been particularly challenging for lithium and cobalt, which were already contending with oversupply.

On the upside though, there has been no shortage of voices calling for a greener post-coronavirus economy, which will fuel EV adoption. Furthermore, a reassessment of the risks of global supply chains could help to fast-track regionalized battery ecosystems. The EV market could actually emerge from the crisis stronger than ever.

According to a recent report by Swiss Resource Capital, the supply of EVs will hardly keep pace with demand once COVID-19 has been overcome. The report finds that the major-economy countries plan to end the sale of petrol and diesel powered vehicles within 10 to 20 years. Within 10 years, Germany, Israel and India plan to end all new sales of such vehicles while the Netherlands, Norway and Sweden are aiming to ban them by 2035. The UK, France and Ireland are planning to end internal combustion vehicle sales of by 2040.

According to a recent World Bank report, production of battery metals will have to increase by nearly 500% by 2050 to meet the growing demand for clean energy technologies. The report says that over 3 billion tonnes of minerals and metals will be needed to deploy wind, solar and geothermal power, as well as the energy storage required to transition to a low-carbon economy. While renewables and energy storage technologies require more minerals, the carbon footprint of their production – from extraction to end-use – will account for only 6% of the greenhouse gas emissions generated by fossil fuels.

Interestingly, Tesla’s Elon Musk said that he plans to manufacture a less expensive, more powerful battery that does not contain cobalt, extending a new, less expensive EV range by 16% compared to the older batteries.

The World Bank report also calls for more recycling and reuse of minerals and notes that even if recycling rates were scaled up for minerals like copper and aluminum by 100%, recycling and reuse would still not be enough to meet the demand for renewable energy technologies and energy storage.

The report also warns of the disruptions the pandemic is causing in global markets and that developing countries that rely on minerals are missing out on essential fiscal revenues but as their economies begin to reopen, they will need to strengthen their commitment to “climate smart” mining principles to mitigate negative impacts.

As mentioned in our previous update, of the various battery types currently in the market place the lithium-ion battery is emerging as a favourite. GlobalData recently said that the increased demand for lithium will spur a corresponding surge in lithium production by 2024. They expect lithium metal production is to reach 134,700 tonnes versus 58,800 tonnes in 2020 and the growth in the lithium market will correlate with greater electric vehicle production and expect that annual EV output will climb to 12.7 million units in 2024 from 3.4 million units in 2020.

China is expected to lead global lithium demand with rising battery manufacturing capacity and EV sales. China remains determined to boost EV sales, targeting a 20% share of the new car sales by 2025, versus just 5% in 2019.

Amid market disruptions in the automotive industry caused by the coronavirus pandemic, S&P Global Market Intelligence forecast global plug-in EV sales to decline by only 3% in 2020, boosted by strong sales in Europe.

“Passenger EV registrations in the European Union in the first seven months surged by 99% year-over-year to 387,000 units, amid a 33% decline in overall passenger vehicle registrations,” S&P analysts said in their September lithium report.

Despite the name, lithium-ion batteries actually require more graphite than lithium as graphite materials remain the dominant active anode material used in lithium-ion batteries.

Roskill sees the graphite industry becoming increasingly focused on the battery market, with growth opportunity for both synthetic and natural and said recently that reduced demand has yet to translate into a major negative price impact on graphite:

“With global recovery expected in the coming months, especially for battery and electrode grades, and Chinese infrastructure stimulus, it seems likely that prices will not suffer in the long term.”

Furthermore, Roskill is expecting total graphite demand over the next 10 years to grow around 5% to 6% per year although they believe environmental costs will continue to play an important role in future supply chain trends and price development, including inspections/closures in China, a call for sustainable battery products and the effects of changing marine fuels on raw material availability for synthetic graphite.

Meanwhile, although some challenges still remain, several research groups are developing rechargeable magnesium batteries which could have the potential to outperform their Li-ion counterparts.

Here in 2020, there are more than 50 electric vehicles for sale or due in the next three model years. Car and Driver magazine recently reported that market research company AutoPacific “counts a remarkable 90 to 100 new electric nameplates coming to U.S. showrooms by 2030.” Then there are EV delivery trucks, busses and semi tractor-trailers.

According to Wintergreen Research Inc., the global electric vehicle market at $39.8 billion in 2018 is projected to reach $1.5 trillion by 2025.

That represents a great deal of battery minerals demand and bodes well for battery minerals explorers and producers. With some jurisdictions planning on banning the sale of internal combustion vehicles, that should be the major catalyst for EV buying.

Nouveau Monde Graphite Inc. [NOU-TSXV; NMGRF-OTCQX; NM9-FSE] has a 100% interest in the advanced Matawine Graphite Project located 130 km north of Montreal, Quebec, which the company is commercializing by building two commercial-scale pilot plant purification modules.

Nouveau Monde Graphite Inc. [NOU-TSXV; NMGRF-OTCQX; NM9-FSE] has a 100% interest in the advanced Matawine Graphite Project located 130 km north of Montreal, Quebec, which the company is commercializing by building two commercial-scale pilot plant purification modules.

Commercial production of carbon-neutral battery grade graphite is scheduled for 2023, making it the largest producer in North America at a time when a graphite shortage is forecast to develop, thus providing a green and reliable alternative to China’s controlled supply chain. With graphite demand exceeding supply by 400,000 tonnes by 2026, there is a projected +500% growth in demand.

It should be noted that U.S. Presidency signed an Executive Order that identified 35 critical minerals that included natural graphite as part of a plan for America to be less reliant on foreign adversaries for essential minerals and metals which, of course, does not include Canada.

Nouveau Monde’s vertical integration strategy will enable it to benefit from the entire value chain from mine to anode materials. To that end, the company’s high-purity graphite products will target high-growth markets such as lithium-ion batteries for electronic devices and electric vehicles, fuel cells, and 5G heat dissipation foils.

At the Matawine high-purity flake graphite property, Measured and Indicated Resources stand at 120.3 million tonnes. An October 2018 Feasibility Study was based on a yearly graphite concentrate production of 100,000 tonnes with a Post-Tax NPV8% estimated to be $751 million and a Post-Tax IRR of 32.2%. The project has an initial CAPEX of $276 million (including a 12.4% contingency) with a Post-Tax payback of 2.6 years. Average sales price of graphite products for the first five years is US$1,532/tonne with life-of-mine price of US$1,730/tonne. OPEX would be $499/tonne. The Matawine mine will be an open pit, truck and shovel operation utilizing all-electric machinery.

At the Matawine high-purity flake graphite property, Measured and Indicated Resources stand at 120.3 million tonnes. An October 2018 Feasibility Study was based on a yearly graphite concentrate production of 100,000 tonnes with a Post-Tax NPV8% estimated to be $751 million and a Post-Tax IRR of 32.2%. The project has an initial CAPEX of $276 million (including a 12.4% contingency) with a Post-Tax payback of 2.6 years. Average sales price of graphite products for the first five years is US$1,532/tonne with life-of-mine price of US$1,730/tonne. OPEX would be $499/tonne. The Matawine mine will be an open pit, truck and shovel operation utilizing all-electric machinery.

Nouveau Monde recently signed an agreement with Olin Corporation, one of the world’s leading chemical companies, for commercial space and to provide chemical supply and site services to support the commercialization of Nouveau Monde’s proprietary thermochemical technology to produce advanced graphite materials.

Conveniently located beside the St. Lawrence Seaway with a rail system and port, Olin’s existing facility in the Bécancour industrial park will be the site for Nouveau Monde to construct two pilot commercial-scale purification furnaces.

Eric Desaulniers, President and CEO of Nouveau Monde, stated: “After four years of technological development, modelling and lab tests with the best universities, engineering firms and international experts, we are enthusiastic at developing our first commercial-scale purification capacity with the support of one of the most respected chemical companies in the world. We have found in Olin, a leading supplier driven by the same values of safety, innovation and environmental stewardship.”

Following completion of a feasibility study in 2021 for a commercial-scale operation, Nouveau Monde plans to launch permitting and construction as early as 2022. The company will target, with its modular approach, 40,000 tonnes annual production of anode material for the initial phase, with the option to reach 100,000 tpa of conversion capacity as demand increases in the battery and speciality markets.

In a recent development, Nouveau Monde advanced its electrification efforts through a partnership with research and industry leaders to develop a new electric propulsion system with a rapid recharging infrastructure adapted to heavy vehicles in the open-pit mining industry. This marks a major turning point in the electrification of heavy vehicles in North America and strengthens Nouveau Monde’s goal of becoming the world’s first all-electric open-pit mine

The prototype is expected to make its first real-world test runs as early as spring 2022 at the Nouveau Monde site.

Nouveau Monde Graphite is extremely well positioned with a long-life, high purity, flake graphite mine, proprietary processing technology, strong institutional and Quebec government support, easy access to customers, inexpensive hydropower and a near-term cash flow at a time of dramatically increasing graphite demand.

Nouveau Monde Graphite recently completed a $20 million financing.

Gratomic Inc. [GRAT-TSXV; CBULF-OTC; CB81-FSE; A143MR-WKN] is nearing completion of construction of its Aukam Graphite Project processing plant in Namibia, Africa. Gratomic holds a 63% ownership of the historic mine site.

Gratomic Inc. [GRAT-TSXV; CBULF-OTC; CB81-FSE; A143MR-WKN] is nearing completion of construction of its Aukam Graphite Project processing plant in Namibia, Africa. Gratomic holds a 63% ownership of the historic mine site.

Custom drying and dewatering equipment has arrived at the Aukam mine site, allowing the company to complete construction of the on-site processing plant, bringing the plant to the commissioning phase with commercial production expected to commence later this fall.

The Aukam graphite mine was previously in production 1940 to 1956 and 1964 to 1974.

Unlike, say, gold or copper, there are different types and grades of graphite. Gratomic is preparing to bring its high-grade, environmentally sustainable, vein graphite products to the North American electric vehicle market and is preparing to introduce its graphite to battery producers for use in advanced anode technology.

A total of 243 kilograms of high-purity graphite concentrate obtained from its pilot testing program is being submitted for characterization for use as anode material in lithium-ion battery cells. The graphite will initially be put through an Air Classification process in Toronto, Ontario and from there will be sent to Dorfner Anzaplan in Germany to undergo spherical micronization and classification. This verification process is expected to establish Gratomic as a leader among its peers in proving that its graphite will be suitable for the anode material supply chain for North American battery manufacturers such as Tesla, Panasonic, and others.

Electric vehicle production is rapidly ramping up significantly with dozens of new models to hit showrooms in the coming years, representing a huge new market for battery minerals. For example, GM is investing US$20 billion to launch 20 new EVs by 2023, including an electric Hummer. Ford is investing US$11 billion in EV manufacturing.

Being naturally of high purity, Gratomic’s vein graphite is ideal for use in this application, requiring simpler, less expensive and more efficient processing methods, resulting in a final product with lower amounts of deleterious elements.

The company will utilize the 23,000 tonnes of historic stockpile at the base of the mountain and intends to move toward an open pit mine sometime in 2021. The 15-km visible strike length of vein graphite on the 1,416 km2 property is in addition to all of the graphite housed within the mountain.

“Gratomic has entered into discussions with several carbon-to-battery experts with the intent to provide a tailored product for the battery market,” said President and CEO Arno Brand.

Gratomic has two off-take purchase agreements for graphite products. Under a US$25 million supply agreement, Gratomic will supply TODAQ pre-graphene graphite. To date, TODAQ has placed two initial purchase orders for 1,800 tonnes of graphite. Another sales agreement has been signed to supply Phu Sumika with 7,500 tonnes of graphite annually for five years that contemplates graphitic products ranging from 80% to 99.9% carbon at prices ranging from US$500 to US$2,800/tonne.

Gratomic has two off-take purchase agreements for graphite products. Under a US$25 million supply agreement, Gratomic will supply TODAQ pre-graphene graphite. To date, TODAQ has placed two initial purchase orders for 1,800 tonnes of graphite. Another sales agreement has been signed to supply Phu Sumika with 7,500 tonnes of graphite annually for five years that contemplates graphitic products ranging from 80% to 99.9% carbon at prices ranging from US$500 to US$2,800/tonne.

Gratomic received its official Mining Licence (ML 215) on May 5, 2020 that includes the processing plant area and the graphite-bearing shear zone of 5,002 hectares. Surface stockpiles will serve as initial feedstock for the first two years of production. Several veins in the lower adit are easily accessible for immediate mining.

Meanwhile, the company has mobilized all three of its 100%-owned drills to execute a strategic diamond drill program targeting areas near known graphite mineralization previously defined by mining, diamond drilling and surface sampling. The program will also incorporate exploratory drilling, testing known structures along strike and optimized targets indicated by recent geophysical surveys.

The company’s management team has extensive experience on a worldwide scale, including planning, engineering, research and development, processing, mine building, project management and sales and marketing. Gratomic Inc. has 71,840.144 shares outstanding.

The company is in a unique position for a junior miner with its business strategy of focusing on mine-to-market commercialization of carbon-neutral, high purity vein graphite. Its near-term production and revenue potential at a mining operation with an expected multi-decade mine life plus a solid growing demand for its graphite products will make it a key player in EV and Renewable Resource supply chains.

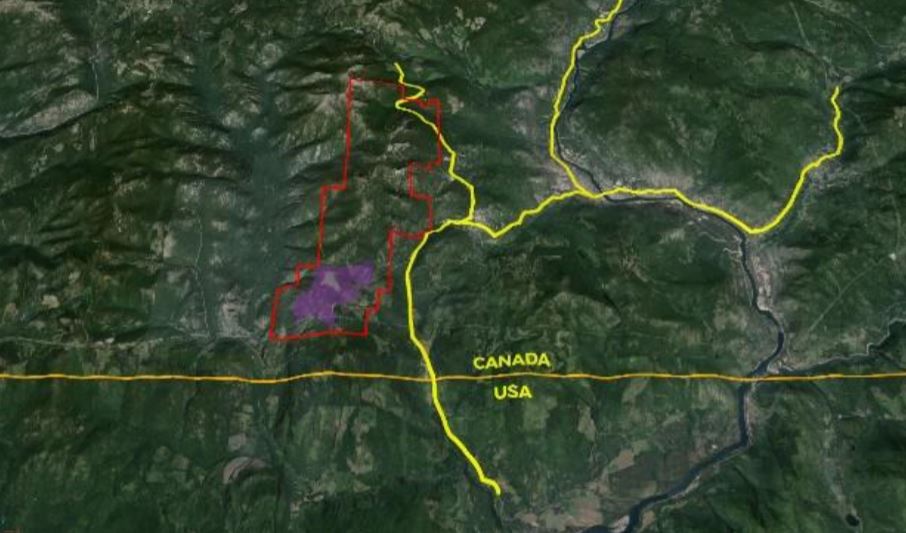

West High Yield (W.H.Y.) Resources Ltd. [WHY-TSXV] has developed its 100%-owned, high-grade Record Ridge magnesium resource asset in British Columbia to an advanced stage as the project moves toward the start-up of the open pit mine. The company’s short-term objective over the next three years is to complete the initial permitting process and begin mining ore in Q3 2021. This project of global significance is one of the world’s largest undeveloped high-grade, green magnesium deposits.

West High Yield (W.H.Y.) Resources Ltd. [WHY-TSXV] has developed its 100%-owned, high-grade Record Ridge magnesium resource asset in British Columbia to an advanced stage as the project moves toward the start-up of the open pit mine. The company’s short-term objective over the next three years is to complete the initial permitting process and begin mining ore in Q3 2021. This project of global significance is one of the world’s largest undeveloped high-grade, green magnesium deposits.

Located near the historic mining town of Rossland in south-central BC, the 8,972-hectare property has NI 43-101 compliant Measured Resources of 28.4 million tonnes grading 24.82% magnesium (Mg), or 41.62% MgO. Indicated Resources stand at 14.6 million tonnes of 24.21% Mg, or 40.15% MgO. These resources represent 10.6 million tonnes of magnesium inside of the company’s 7.5 km2 outcrop discovery.

The figures are based on 10,000 metres of drilling in 77 holes, all of which were mineralized.

Magnesium mineralization remains open along strike on company land and to depth.

An independent Preliminary Economic Assessment has demonstrated robust project economics for a 3,000 tonne-per-day open pit operation with an After-Tax NPV5% of CDN$742 million and an After-Tax IRR of 30% over a 42-year mine life. Upfront CAPEX requirements total CDN$310 million. Payback is three years. As process optimization and increased market pricing develop, the economics of the asset development will be further enhanced.

A market study supports premium MgO pricing. Magnesium demand is increasing with many applications including automotive, aerospace, defense, fertilizer, MG cement, pharmaceuticals, magnesium batteries, wallboard, pure magnesium metal and alloys. The global high-purity magnesium oxide market has CAGR projections ranging from 6% to 12% in the next 10 years.

Magnesium is one of the 35 strategic/critical minerals needed for the U.S. economy and national security. Currently, the North American magnesium compounds markets rely on over 50% imports.

In 2019, the company completed its Environmental Assessment and Environmental Baseline Study and submitted its Mine Plan Permit Application that is expected to be received in the near future. The proposed mine plan envisages a conventional truck and shovel operation with primary and secondary crushing on site before being transported to a processing facility location yet to be determined. Discussions with various magnesium refiners is ongoing with the objective to secure buy forward agreements one of the key commercial aspects of the company’s plan.

In 2019, the company completed its Environmental Assessment and Environmental Baseline Study and submitted its Mine Plan Permit Application that is expected to be received in the near future. The proposed mine plan envisages a conventional truck and shovel operation with primary and secondary crushing on site before being transported to a processing facility location yet to be determined. Discussions with various magnesium refiners is ongoing with the objective to secure buy forward agreements one of the key commercial aspects of the company’s plan.

Micro-plant process testing has been underway with optimized positive results that will significantly reduce capital costs and improve project economics. The company has developed a proprietary hydrometallurgical process with the KPM Lab in Kingston, Ontario for producing premium (>99%) MgO and Mg(OH)2 products with nickel and silica by-products. This is a closed loop “green” process with no waste and little to no emissions.

West High Yield plans to build a high-purity, 2 tonne-per-hour MgO demonstration plant in next year using its proprietary process. The plant would annually process over 16,000 tonnes of Mg ore and produce over 6,000 tonnes of high-purity MgO with gross revenue of over $11 million. The demonstration plant would continue operating until commissioning of the first commercial plant. Operations at a commercial level are currently scheduled for the first quarter of 2024 that would provide feed for multiple magnesium refineries.

To implement their objectives, West High Yield is raising more funds. These non-brokered private placements include $1.5 million to complete the Final Mining Permit as well as $3.5 million to complete the final mine design and operational plans for a Q3 2021 start; finalize pilot and main plant design; initiate organizational structure and hire key staff; complete a 22-hole gold drill program that will be expanded; complete preparation work and award a mining contract for the 2021 season. The company will then apply to increase throughput to 1 million tonnes per year and either purchase or lease a Brownfield plant site. Community engagement activities will continue.

During 2021, West High Yield has plans for major financings, including $50 million in Q1 2021 and $250 million in Q3 2021. Part of these funds will be used for building infrastructure for the MgO processing plant and, in concert, build a clean room/laboratory for pharma/medical grade MgO production.

Frank Marasco, Jr., President and CEO, says that the company would consider a suitable partnership, JV operator or takeover offer to complete the project. He says that there is an addressable market potential for wallboard, ingots, batteries, fertilizer, and cement plants.

Located in a well-established mining district 3 km north of the U.S. border, there is excellent infrastructure nearby, including CP Rail, highways, secondary roads, electrical power, water, related support services and natural gas.

West High Yield has other projects in British Columbia. The company has received it permit for a 20,000-metre drill program on its past-producing Rossland Gold Camp property where an earlier drill program returned 25.16 g/t gold over 4.6 metres and 40.11 g/t gold over 4.1 metres.

West High Yield has 66,892,820 shares outstanding.

With the advanced Record Ridge Magnesium, Mine at the construction stage and a growing demand for its products, plus nearby gold projects, West High Yield Resources represents a substantially de-risked unique opportunity for investors.

Neo Lithium Corp. [NLC-TSXV; NTTHF-OTC] is moving to establish itself as a key player in the global battery metals sector by developing one of the world’s largest lithium brine projects Argentina.

Neo Lithium Corp. [NLC-TSXV; NTTHF-OTC] is moving to establish itself as a key player in the global battery metals sector by developing one of the world’s largest lithium brine projects Argentina.

Neo Lithium’s 100%-owned Tres Quebradas (3Q) Project is a unique high-grade lithium brine lake and salar complex, situated in Catamarca, Argentina, a region known as “Lithium Triangle.” This area host over 60% of the lithium resources of the world and encompasses Argentina, Chile and Bolivia.

A key feature of the project is an unusually high grade and low level of impurities that should allow Neo Lithium to develop a project that will rank much lower on the cost curve than other comparable operations.

Lithium is the key ingredient in the production of lithium-ion batteries used in electric vehicles as well as electronic devices such as smart phones and laptops. Lithium is also used in the production of heat-resistant glass and ceramics, lithium grease lubricants, iron, steel and aluminum.

The Toronto-based company is developing the 3Q Project amid reports that demand for the electric vehicle battery will likely triple over the next five years as automakers shift their focus away from internal combustion engines to electric vehicles.

It is a project which has already attracted the attention of Contemporary Amperex Technology Co Ltd. (CATL), a Chinese company which supplies lithium ion phosphate batteries to electric car maker Tesla Motors Ltd. [TSLA-NASDAQ]. CATL is also supplying different types of batteries to various other carmakers including Daimler AG, and Toyota Motor Corp.

It is a project which has already attracted the attention of Contemporary Amperex Technology Co Ltd. (CATL), a Chinese company which supplies lithium ion phosphate batteries to electric car maker Tesla Motors Ltd. [TSLA-NASDAQ]. CATL is also supplying different types of batteries to various other carmakers including Daimler AG, and Toyota Motor Corp.

CATL would become Neo Lithium’s second largest shareholder with an 8.0% equity stake after recently agreeing to buy more than 10 million shares at 84 cents each, raising Neo Lithium’s cash position from $29 million as at June 30, 2020 to approximately $37 million.

On October 23, 2020, Neo Lithium shares were trading at 99 cents in a 52-week range of $1.23 and 38 cents, leaving the company with a market cap of $116.3 million based on 117.5 million shares outstanding.

Brines (in salt ponds) and spodumene (hard rock) represent the two main sources of commercial lithium production. The largest known deposits of brine resources are found in South America’s lithium triangle.

Neo Lithium has already shown that it can produce battery grade lithium carbonate in their own pilot plant using concentrated brine from 3Q project ponds.

A prefeasibility study (PFS) done in 2019 concluded that simple evaporation with minimal reagents, combined with an industry standard carbonation process can obtain Lithium Carbonate Battery Grade from the brine. The operation cost is going to be one of the lowest in industry.

At the 3Q Salar Site, brine will be extracted from wells and evaporated to 3.4-3.8% lithium. This concentrate will be trucked to a site at the town of Fiambalá (160 km from the project) for further processing to remove impurities, carbonation, drying and packaging. The final stage involves rail transportation to a port in Buenos Aires.

The PFS envisages a low initial capital expenditure of $318.9 million and that the project will be positioned at the lower end of the operating cost curve.

CATL’s involvement in project like this should come as no surprise as China is currently the largest consumer of the white metal and the world’s largest maker of electric vehicles.

CATL has indicated that it will help Neo with the feasibility study for its 3Q Project, provide technical support on the downstream production, and potentially support and participate on the final financing package. This kind of support will help Neo attract more investors and firm up a time line for the opening of a project that the company hopes will initially produce 20,000 tonnes of battery grade lithium carbonate annually over a 35-year project life and have to potential to expand its capacity to 40,000 tonnes.

Neo Lithium is already employing an experienced local technical team of over 10 engineers and 60 professionals. Its founders were also the discoverers of another lithium project -Â Cauchari – now a mine in construction. 3Q is the second project that this technical team is putting together to be the next major lithium producer.