Record high lithium prices to fuel demand for property acquisitions

By Peter Kennedy

Some of the world’s leading mining companies are moving to capture the opportunity offered by rising demand for lithium.

Benchmark Mineral Intelligence reported on October 13, 2022, that lithium prices in China hit an all-time high of US$74,475 a tonne as battery manufacturers scramble to secure supply amid booming demand from the electric vehicle market. Prices have more than doubled so far in 2022.

Benchmark said prices for lithium hydroxide, which is used in batteries with high nickel content is up nearly 150% this year, trading at US$73,925.

Benchmark said prices for lithium hydroxide, which is used in batteries with high nickel content is up nearly 150% this year, trading at US$73,925.

Strong demand for the soft silvery metal is attributed to its key role in the in the production of lithium-ion batteries, which are used in small electronic devices, including smart phones, laptops, and electric vehicles

Based on the assumption that electric vehicles make up around 40% of new passenger car sales by 2030, United Kingdom-based energy consultant Wood Mackenzie predicts that nearly 800,000 tonnes of Lithium Carbonate Equivalent (LCE) of additional lithium would need to come online in the next five years to meet future demand.

Lithium is also a key in ingredient used in the production of heat-resistant glass and ceramics, lithium grease lubricants, iron, steel and aluminum.

Record high prices and expectations of rising demand have convinced companies like Rio Tinto Plc [RIO-NYSE], Argosy Minerals Ltd. [AGY-ASX] and Argentina Lithium & Energy Corp. [LIT-TSXV] to pick up lithium projects in Argentina’s prolific lithium Triangle, an area that produces about half of the world’s lithium.

“We saw the lithium market heating up and we decided to put together some projects with evidence of lithium,’’ said Argentina President and CEO Nikolaos Cacos.

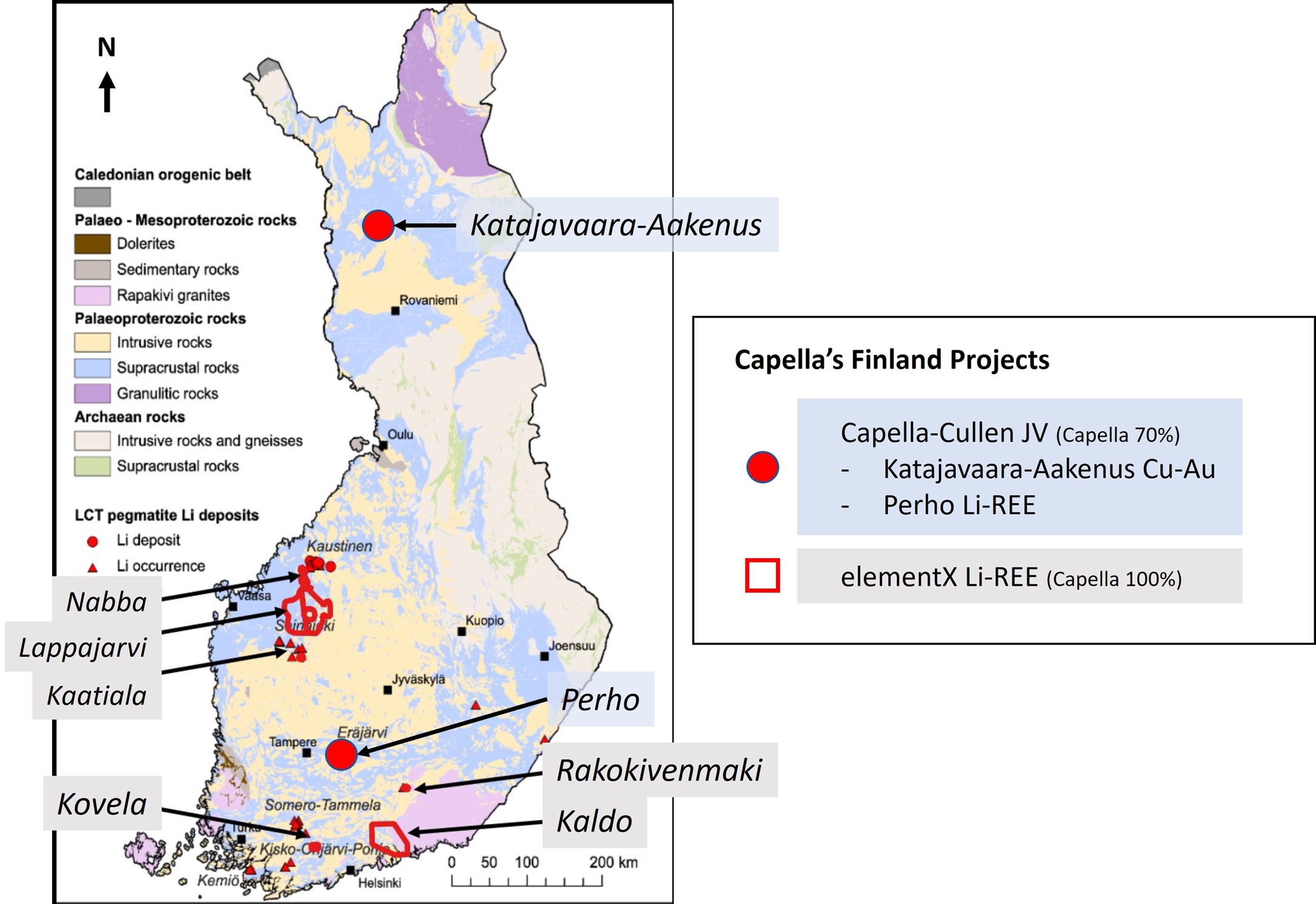

Capella Minerals Ltd. [CMIL-TSXV, N7D2-FRA] recently expanded its portfolio of lithium-REE (rare earth element) and copper gold projects in Finland by striking a deal with elementX Finland Oy for the acquisition of a portfolio of seven lithium pegmatite and rare earth element reservations.

The main sources of lithium for commercial extraction are localized hardrock pegmatites (igneous rocks of post magmatic fluids) and continental brines (saltwater aquifers). Of the various ores found in pegmatite, spodumene ore is generally the most economically viable source of lithium.

The spodumene mine in Greenbushes, Western Australia, is the largest active lithium mine in the world. The ore mined from this facility exhibits the highest concentrations of lithium oxide (Li20) available.

However, over the past 40 years, brines have become a viable alternative to spodumene mining. Brines, which are salty, mineral-rich solutions occurring in aquifers, are typically found in regions with specific geological conditions.

The first large-scale extraction of lithium brine occurred in Clayton Valley (Silver Peak, Nevada) in 1966. Albemarle Corp.’s [ALB-NYSE] Silver Peak lithium mine is North America’s only lithium brine operation.

Lithium-rich brines are also found throughout South America, in the Central Andes region. However, these brine deposits referred to as “salars,” vary substantially in terms of lithium concentrations and mineral compositions and are exposed to different weather conditions., all of which influence the ability to economically recover lithium from each salar.

Actively producing salars on a commercial scale include the Salar de Atacama in Northern Chile, and the Salars del Hombre Muerto and de Olaroz in northwestern Argentina. Of these, the Salar de Atacama exhibits the highest lithium concentrations and the most favourable extraction conditions of any brine resource in the world.

When Rio Tinto acquire Rincon Mining Pty. Ltd, which owns the Salar de Rincon Project in Argentina in December, 2021, it said the Rincon project holds the potential to deliver a significant new supply of battery-grade lithium carbonate, to capture the opportunity offered by the rising demand driven by the global energy transition.

Rio Tinto has said the direct lithium extraction technology proposed for the project has the potential to significantly increase lithium recoveries as compared to solar evaporation ponds. A pilot plant is currently running at the site and further work will focus on continuing to optimise the process of recoveries.

Eyeing a similar opportunity, Argosy Minerals has commenced construction of a 2,000 tonne per annum processing plant (pilot plant) on its nearby Rincon project after outlining a resource of about 245,000 tonnes.

Pending successful development and production from the pilot plant, the company will consider the best development pathway to ultimately target commercial production from the project and earn its ultimate 90% interest in the joint venture entity.

There are many other sources of brine being evaluated by various companies focused on lithium extraction, including the Salar de Antofalla, the Salar de Maricunga in Chile, the Salar de Uyuni in Bolivia, and Qaidam Basin in China and Zhabuye Lake in Tibet.

Brine containing high concentrations of lithium is pulled from saltwater acquifers using extraction wells. From the wellhead, the brine is diverted to an evaporation pond system. Using solar evaporation, the lithium salts are concentrated in the brine and eventually routed to the next pond in the system. The step is continued multiple times, until the lithium concentrate reaches a level high enough for conversion to lithium carbonate or lithium hydroxide.

There are other means for lithium extraction from brines using absorbents or chemical extraction, but these processes have yet to be proven on a commercial scale.

Capella Minerals Ltd. [CMIL-TSXV, OTCQB-CMILF, N7D2-FRA] recently expanded its portfolio of lithium-REE (rare earth element) and copper gold projects in Finland by striking a deal with privately owned elementX Finland Oy for the acquisition of a portfolio of seven reservations covering lithium (spodumene-bearing) pegmatites and rare earth element occurrences.

Capella Minerals Ltd. [CMIL-TSXV, OTCQB-CMILF, N7D2-FRA] recently expanded its portfolio of lithium-REE (rare earth element) and copper gold projects in Finland by striking a deal with privately owned elementX Finland Oy for the acquisition of a portfolio of seven reservations covering lithium (spodumene-bearing) pegmatites and rare earth element occurrences.

Capella said the elementX projects are predominantly on lithium-cesium-tantalum (LCT) pegmatite complexes located within the Jarvi-Pohjanmaa and Seinajoki lithium-permissive tracts as defined by the Geological Survey of Finland (GTK. Four of the projects being acquired are located adjacent to Kelibre Oy’s mine development at Kaustinen, where first commercial spodumene production is currently scheduled for 2024.

Accordingly, the company says it will be extremely well placed to participate in the global electrification and decarbonization process.

“These are the right metals at the right time,’’ said Capella President and CEO Eric Roth during an interview with Resource World. Subject to TSV Venture Exchange approval, elementX will take a 9.9% stake Capella in return for reservations (properties) which cover 4,000 square kilometres and come with exclusive exploration rights lasting an initial two years.

Speaking in an interview from Spain, Roth said he is confident that the properties contain significant lithium-bearing pegmatites. His aim is to zero in on the ones that are likely to be the most economic to develop.

“We would be targeting about five to ten million tonnes of greater than 1% Li20,” he said.

In overview, the elementX acquisition is expected to provide Capella with a significant opportunity to be a major player in the growth of lithium and REE production in Finland, which itself has the potential to become one of the EU’s major sources of these desired commodities.

On September 14, 2022, the European Commission outlined the creation of the European Critical Raw Materials Act (ECRM), which is designed to support the development of a resilient European supply chain of both lithium and REES. Initial targets indicated in the ECRM Act are that at least 30% of the European Union’s demand for refined lithium by 2030 should be sourced from the EU itself (in addition to at least 20% of REE demand).

On September 14, 2022, the European Commission outlined the creation of the European Critical Raw Materials Act (ECRM), which is designed to support the development of a resilient European supply chain of both lithium and REES. Initial targets indicated in the ECRM Act are that at least 30% of the European Union’s demand for refined lithium by 2030 should be sourced from the EU itself (in addition to at least 20% of REE demand).

In parallel, the Norwegian government is also supporting the construction of the country’s first lithium-ion battery plant in the northern city of Mo I Rana. This battery plant, which is currently expected to enter production in 2025, is part of a broader government strategy to take advantage of the abundance of low-cost renewable (hydroelectric) energy in-country and become a major contributor to the future of global lithium battery production.

Meanwhile, Capella said it has initiated a non-brokered private placement of up to 10 million units priced at $0.06 per unit, for gross proceeds of $600,000. The company said it has secured initial commitments for $300,000, of which $150,000 has been committed from an elementX shareholder.

Each unit of the private placement shall consist of one common share and one-half of a share purchase warrant, which each whole warrant entitling the holder to purchase one additional common share for 12 cents per share at any time within two years from the date of issuance. The warrants are subject to an accelerated exercise clause in the event the company’s share price exceeds 25 cents for 10 consecutive trading days.

Each unit of the private placement shall consist of one common share and one-half of a share purchase warrant, which each whole warrant entitling the holder to purchase one additional common share for 12 cents per share at any time within two years from the date of issuance. The warrants are subject to an accelerated exercise clause in the event the company’s share price exceeds 25 cents for 10 consecutive trading days.

Proceeds of the private placement are earmarked for exploration at the company’s enhanced portfolio of lithium and rare-earth element (REE) projects in Finland and high-grade copper-cobalt projects in Norway.

In Norway, the company’s current focus is on the following copper-cobalt projects:

- The advanced exploration-stage Hessjogruva copper-cobalt project and adjacent Kongensgruve and Kjoli projects in the Roros mining district, Trondelag County;

- The discovery of new high-grade copper-cobalt deposits in a district-scale land position around the past-producing Lokken (Lokken Verk District) copper mine, Trondelag County;

- The discovery of new copper-cobalt deposits in former Vaddas-Birtavarre mining district in northern Norway.

The focus on cobalt coincides with rising demand for “ethically sourced” cobalt, and Capella’s desire to offer the market an alternative to the Democratic Republic of Congo, which currently accounts for roughly 60% of the world’s cobalt production.

On October 26, 2022, Capella shares were trading at $0.065 in a 52-week range of 11 cents and $0.04, leaving the company with a market cap of $9.8 million, based on 151 million shares outstanding.

Argentina Lithium & Energy Corp. [LIT-TSXV] is a company that offers low risk exposure in resource development in the highly prospective Argentinian portion of the fabled Lithium Triangle.

It is a region that contains 60% of the world’s known reserves of lithium, a soft silvery metal that is an essential ingredient in lithium-ion batteries for hybrid and electric cars, as well as rechargeable power for laptops, phones and other devices.

Argentina Lithium has secured a large property position in the Lithium Triangle, thanks to its membership in the Grosso Group, a resource management group, based in Vancouver that has pioneered exploration in Argentina since 1993.

The company is exploring for lithium-rich brines, which can be found in South America and are often referred to as “salars,” or salt flats.

It has 57,000 hectares of claims on four salars in pro-mining and adjacent provinces of Salta and Catamarca. These are road accessible properties that tie Argentina Lithium to the electric vehicle revolution that is helping to drive global demand for lithium, recently sending prices to record highs.

The portfolio includes the Antofallo North Project, which covers 15,000 hectares of claims located 20 kilometres west of Argentina’s largest lithium producing operation at Salar de Hombre Muerto.

The southern boundary of Antofalla North is located approximately 500 metres north of properties held by Albemarle Corp. [ALB-NYSE], a global leader in lithium production. Albemarle has stated that the lithium resource on its Antofalla property has the potential to be certified as the largest lithium resource in Argentina.

Believing that the time was right to expand its portfolio, Argentina Lithium recently signed a letter of intent acquire 100% interest in two properties located in the heart of the prolific lithium district in Salta Province. They are the 2,370-hectare Rincon West, and 15,857-hectare Pocitos properties.

“These properties represent prime exploration assets with infrastructure close by and potential for discovery of high-grade lithium brines,” said Argentina President and CEO Nikolaos Cacos.

Salta is a pro-mining jurisdiction and Argentina Lithium intends to fast-track drilling to evaluate and advance these well-located properties,’’ said Cacos

The Rincon West prospect is a single mining concession, located on the west side of the Rincon Salar. There are two significant lithium resource development projects on the salar, owned by Rio Tinto Plc [RIO-NYSE], Argosy Minerals Ltd. [AGY-ASX], both of which have executed demonstration scale production of lithium carbonate.

Rio Tinto acquired its Rincon lithium project for $825 million in December 2021 and has agreed to provide Ford Motor Co with lithium from this salar.

Due to the fact that Rio Tinto and Argosy have both outlined significant lithium resources and are moving towards production on their nearby projects, Argentina Lithium has chosen to place its initial focus on Rincon West.

In a press release on May 31, 2022, the company said it had commenced exploration drilling at Rincon West, saying it planned to complete five exploration holes to test multiple prospective brine targets identified from geophysical survey data announced in a news release on May 2, 2022.

Subsequently, on October 25, 2022, the company reported positive lithium brine values from the third and fourth diamond drill holes at the project. The fifth exploration hole is currently in final steps to completion.

“The fourth exploration hole has produced our best results to date. Lithium brines start at 38 metres depth, but the exciting result is the interval from 95 metres to 227 metres, with lithium values ranging from 334 to 382 mg/litre over a continuous 132-metre interval. The third hole, located in the southern portion of the property produced lower grade brines at the bottom of the hole.

Though the lithium potential appears to decrease in the southern portion of the basin, it is notable that we still produce lithium brines while stepping out 1.8 km south from our previous drilling. We have more drilling to do, to fully delineate our brine aquifer, particularly in the west and north.” stated Miles Rideout, V.P. of Exploration.

On October 3, 2022, Argentina Lithium reported positive lithium brine values from the second drill hole at Rincon West.

“The results of the second exploration hole demonstrate remarkably consistent lithium grades, when compared to the first,” the company said. RW-DDH-002 results reveal an impressive, concentrated brine aquifer, tested with packer sampling over 77% of the interval between 182 and 305 metre depths, with lithium values ranging from 337 to 367 mg/litre. Additional concentrated brines with lower lithium contents were also recovered from this 118-metre interval.

Drilling thus far validates that the adjacent lithium salar extends under our properties, with consistently high lithium grades. The drill program will continue as planned with the aim of delineating an initial lithium mineral resource,’’ said Miles Rideout, Vice-President, Exploration at Argentina Lithium.

The company’s drilling permit allows for up to nine exploration holes; thus, the scope of the program may be expanded based on results.

On October 26, 2022, Argentina Lithium shares were trading at 28.5 cents in a 52-week range of 96 cents and 19.5 cents, leaving the company with a market cap of $25.8 million, based on 90.7 million shares outstanding.